Monthly commentary

Monthly Musings: Summer lull – a thing of the past?

What an eventful summer. No, not the Euros. Or the Olympics. Or Wimbledon. Nor do we mean the political shenanigans – in the US, France, and of course, the UK.

For once, in the normally dead days of summer, we’re talking about the financial markets.

There’s a reason why clichés exist; they might be corny or tacky… but there’s usually a dollop of truth in them. August brought a couple of old favourites out again, highlighted below.

Early into August, stock markets crashed. It wasn’t pretty: the VIX index – a measure of volatility in the S&P 500 – spiked to levels only last surpassed by the levels during Covid-19.

Anxiety ran high. It’s impossible to pinpoint what specifically triggered the crash, or the quantities each of the ingredients that made for this secret recipe contributed to it. Stocks take the stairs up and the lift down.

But some educated guesses suggest a mix-and-match of events: slightly weaker-than-expected US job growth and a rise in unemployment (many believe this was the trigger); in Japan, the central bank’s decision to raise the interest rates didn’t land well with those borrowing at low interest rates to invest in higher-yielding assets elsewhere (the so-called yen carry trade).

In isolation, none of these events were so dramatic. In fact, even combined, there is hardly a strong, compelling reason to believe the stock market could crash on the back of slightly weaker-than-expected data. But once that lift starts moving, you can be in the basement in no time.

...of course, things turned around so quickly that investors looking to buy when there’s blood in the streets didn’t even get the chance to. A week after the fall, the streets were spotless, and things were back to normal!

Towards the later part of August, eyes turned to Nvidia as it prepared to disclose its earnings. Goldman Sachs has described the chipmaker as the most important stock on the planet.

But when Nvidia disclosed its financial results, it turned out that good news can also be bad news. The results themselves were unbelievably good. 122% year-on-year sales growth; $30 billion dollars in sales in just the second quarter!

Boom! Nvidia’s shares drop more than 8% on announcement. Why? The results weren’t good enough. Expectations were unrealistic. For a world fixated on AI, spectacular growth has become ordinary. Putting an unreasonable amount of hope into one stock can only be risky.

Of course, at least individual stockpickers (whether seasoned professionals or Reddit-led amateurs) have made a decision to buy into Nvidia’s hype (or not).

The big problem is for passive investors. With a market cap of more than $3tr, Nvidia has a weight in the S&P 500 index of more than 6%. They’ve no control over whether they own Nvidia or not – perhaps they don’t even know!

As we see it, concentration is hardly ever a good thing. And Nvidia might be an important stock, but there are many others worth looking at. Remember: it’s not a stock market, it’s a market of stocks. You don’t have to buy all of them, and certainly not at the same size as everyone else!

Because over the month as a whole, the market remained quite calm. Maybe the macroeconomic background was not as strong as some had hoped, and, sure, the largest stock on Earth didn’t deliver.

And yet, one of the oldest concepts in investing prevails: not putting all your eggs in one basket. Blending stocks with lower risk bonds worked. Spreading risks around the world worked. Avoiding extreme concentration in any one industry worked. Diversification worked.

August Markets Wrap

August kicked off with a 0.25% interest rate cut from the Bank of England in a tight vote that suggested some members of the Monetary Policy Committee are wary of weaker spots in the economy.

In any case, the Bank had two options: (1) to adopt an optimistic stance, emphasising the signs of improvement of recent inflation figures, or (2) to adopt a more sceptical view, placing more emphasis on the economy’s struggles to emerge from a shallow recession.

It chose option (1). And later in the month the Bank’s optimistic decision was validated by upbeat inflation figures for July. The lower-than-expected overall figure was owed to slowing headline and services inflation, the latter of which has been a concern for the economy given its stubbornness.

In the same week, other major central banks moved in different directions. The Bank of Japan increased the interest rate to 0.25%, and it has more recently signalled that, under the condition of conducive inflation rates, it could raise rates further.

While the Federal Reserve kept rates on hold, chair Jerome Powell said cuts could begin as soon as September. The markets immediately moved to price in three rate cuts before the end of the year, which combined with the release of favourable economic data, sent US government bonds on a rally.

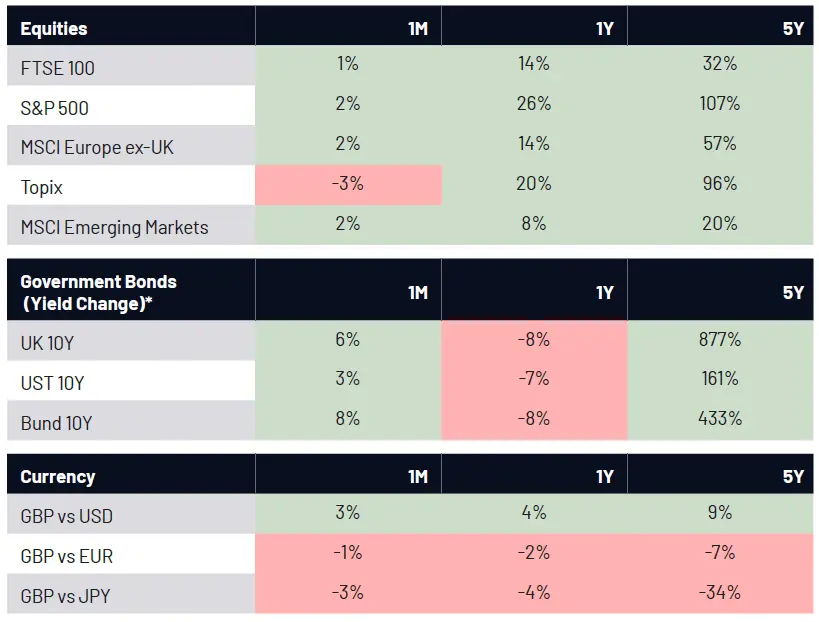

Market Moves

Source: Bloomberg. Data as of 2 September 2024.

*Prices fall when yields rise, so formatting is inverted

What we’re watching in September:

- 11 Sep: US CPI

- 18 Sep: UK CPI

- 19 Sep: US Federal Reserve’s interest rate decision

- 19 Sep: Bank of England’s interest rate decision.

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.